If you’re reading this on your phone after a long day, chances are you’re tired—not just from work, but from pretending your money is under control when it really isn’t.

You see your salary come in, then disappear.

Your parents say, “Just be careful,” but no one tells you how.

And by the end of the month, you’re again asking, “Where did all the money go?”

You’re not lazy.

You’re not stupid.

You’re just stuck in a few silent habits that slowly eat your wallet while you’re not even watching.

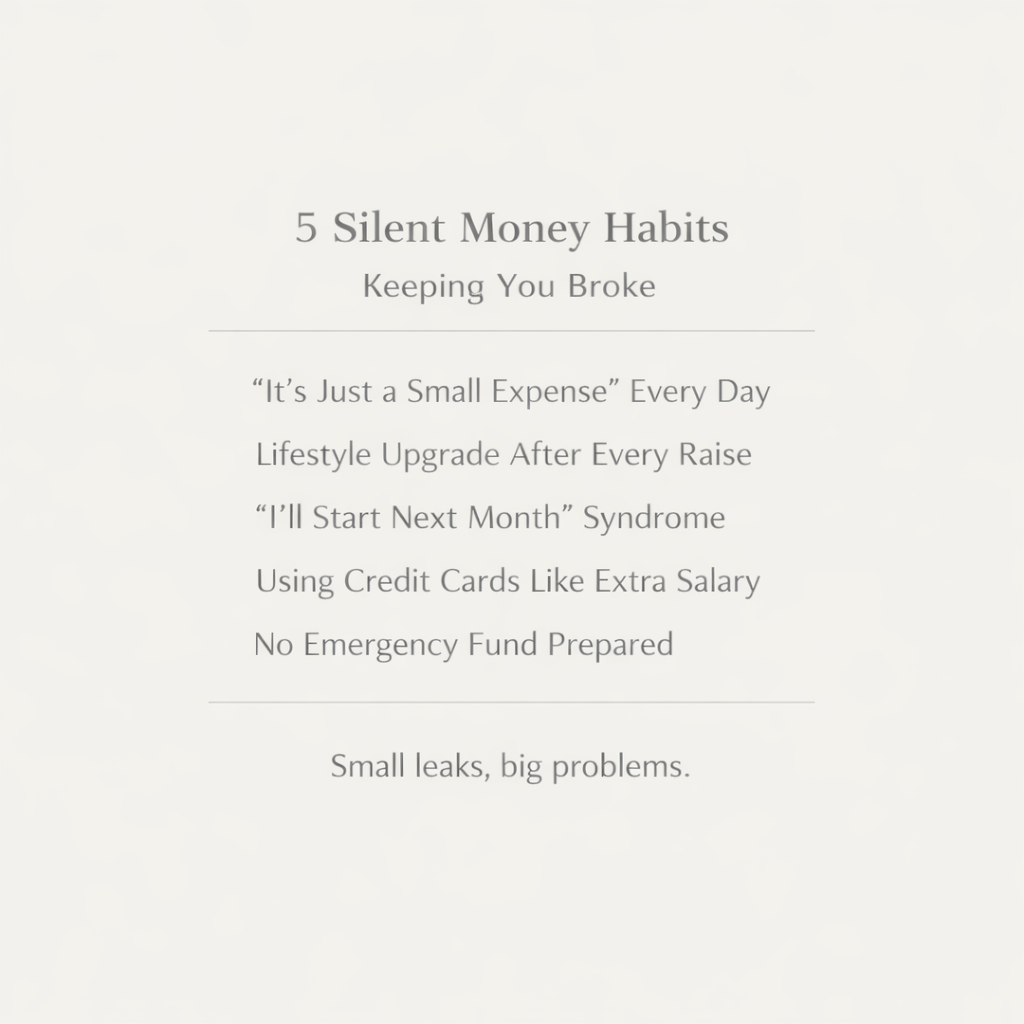

1. “It’s Just a Small Expense” Every Single Day

You hear it all the time:

“Chai ₹10, samosa ₹20, ola ₹50… it’s just a little.”

But do this math:

- ₹50 for chai/snacks per day →

₹1,500 per month

₹18,000 per year

That’s more than a 1‑month EMIs on many phones or bikes.

And this is just one habit.

Try this instead:

Pick one category (like daily snacks or autos) and cut it by 50% this month.

Save the rest in a separate account or even a separate UPI wallet.

Soon you’ll see how “small” things can literally buy you freedom.

2. Keeping the Same Lifestyle After Every Salary Hike

You finally get that promotion or increment.

Your first thought:

“Ha! Now I can upgrade my phone / bike / gym / clothes.”

Job done.

Debt level: same.

Here’s the truth:

Every time your income goes up, your expenses also go up—but no one tells you that.

You’re richer on paper, but your stress level stays the same.

Try this:

Next time you get a raise, do this:

- Cut 50% of the extra money for savings or debt.

- Only spend the other 50% on lifestyle.

In 6–12 months, you’ll have a real cushion, not just a fancier phone.

3. “I’ll Start Next Month” Syndrome

You’ve heard it a thousand times:

“I’ll start investing next year.”

“I’ll control expenses next month.”

But next month, life happens:

- relatives visiting,

- emergencies,

- “it’s just this once” gifts and events.

And suddenly, next month never comes.

Money doesn’t work like mood.

It works like habit.

If you don’t build the habit today, you’ll never magically become “disciplined” one fine day.

Start small:

- ₹100 per day in a savings fund or SIP.

- Track just 1 week of your real spending (no cheating).

You’ll be shocked at what you discover.

4. Using Credit Cards Like Extra Salary

Credit cards are dangerous because they feel safe.

You pay ₹10,000, then next month you pay ₹200.

“Easy, no stress.”

But that ₹10,000 is not gone.

It’s just postponed… with interest.

Soon you’re paying more for interest than for what you actually bought.

If you must use a card:

- Only for fixed, planned spends (like laptop, medicine, etc.).

- Pay the full bill on time every month.

Never, never roll it over.

If you can’t pay it full this month, don’t buy it.

5. Ignoring “Emergency Fund” Like a Myth

Most people only think about emergencies after they happen.

Medical issue?

Job loss?

Bike breakdown?

Suddenly everyone is asking for help.

If you ask any normal person in Lucknow, Delhi, or Mumbai:

“Do you have an emergency fund?”

Most will laugh and say, “Haan, par kuch bhi nahi.”

Here’s a simple rule:

Try to save at least 3–6 months of your basic living expenses.

Start small:

- ₹1,000 this month,

- ₹2,000 next month,

- and keep growing it.

Soon you’ll stop feeling like a one‑accident‑away victim of life.

Street‑Style Money Rule (Easy to Remember)

Think of your money like tap‑water:

- If you leave the tap open all day, the bucket will never fill.

- Same with your money:

If you keep small leaks open every day, you’ll never see real savings.

So, choose 1 leak today:

Maybe daily snacks.

Maybe unnecessary online orders.

Maybe keeping an expensive subscription “just because it’s there.”

Close that leak.

Watch what happens in 3 months.

Finally,

You don’t need to be an MBA to handle money.

You just need to stop ignoring the small habits that quietly drain your life.

If this made sense, do this:

Save one practical tip from this article and act on it this week.

That’s all it takes to start shifting from “stuck” to “in control.”

Comments (0)

Sign in to leave a comment